Credit union members and their households really like credit unions. They exhibit high levels of trust in credit unions, preferring credit unions over all other providers of financial services. And they tell us they would prefer to do all of their family’s financial business at their credit union, if the credit union could meet their full range of needs.

But very few members look to their credit union for financial advice. Among credit union member households that have a primary financial advisor, only 5% fill that role with an advisor that works in a credit union.

In fact, more credit union households consider a bank-based advisor to be their primary advisor (6%) than pick a credit union advisor for the job. That is according to the biennial Macromonitor survey1, which encompasses a nationally representative sample of 4,320 households including detailed financial and other data for 2,057 households with a credit union member.

What can credit unions do to position themselves as primary advisor for more of their members? The data in the Macromonitor suggest that credit unions should focus on taking the following steps:

- Prepare the household’s financial plan

- Preparing the household’s financial plan appears to cement the advisor’s position as the household’s primary source of advice

- 99% of households with a financial plan prepared by a credit union or bank consider a credit union or bank advisor to be their primary advisor

- Capture the majority of the household’s savings and investments

- Households that consider a credit union or bank advisor to be their primary financial professional keep 63% of the household’s savings and investments with that institution, on average

The path to primacy runs through financial planning and asset accumulation. For a client to consider a firm as their primary financial provider, the firm needs to have provided a written financial plan and gathered most of the client’s investible assets. If more credit unions can hit these important benchmarks with more of their members, the share that look to credit unions as their primary source of advice will grow.

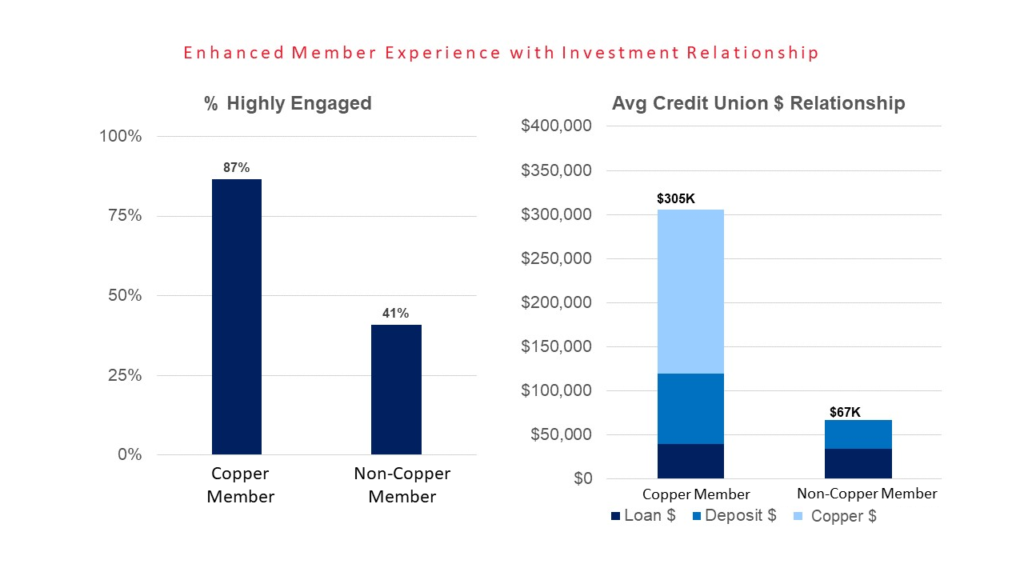

The national survey data are consistent with the experience at CommunityAmerica Credit Union, where members who are clients of its broker dealer subsidiary, Copper Financial Network, LLC (CuFi), are twice as likely to be highly engaged as members without a CuFi relationship. Moreover, members with a CuFi relationship have twice the deposit and loan balances, and keep almost eight times more assets at CommunityAmerica, counting assets administered by CuFi.

The good news is CuFi currently works with credit unions across the country to help produce this impact for its partners by offering them a breadth of investment services.

As CuFi is credit union owned they understand the unique needs of credit union members. You are not a number, and service levels are completely flexible and tailored to each credit union’s unique needs. Additionally, CuFi has built a best-in-breed technology experience for its partners, including an award-winning technology platform through Apex Clearing. All help ensure the level of service provided to members is what they have come to expect from their credit union.

If you are a credit union and would like to learn more about how you can partner with CuFi, please contact our Chief Operating Officer, Justin Steitz, at jsteitz@cu.financial or (913) 905-8192.

1 2016-2017 MacroMonitor, Strategic Business Insights