Kehrer Bielan research has found that financial planning is a win, win, win for the member, the advisor, and the credit union. Members with a plan are more confident about their financial future, move more of their assets to the advisor who works with them on the plan, and are less likely to abandon the credit union to seek financial advice elsewhere:

- Almost half of households with a financial plan express a great deal of confidence in their financial future, twice the rate of the general population.

- Households with a financial plan provided from a financial institution keep 85% more of their savings and investments there.

- 99% of households that have a financial plan provided through a credit union or bank consider the institution to be their primary financial advisor.

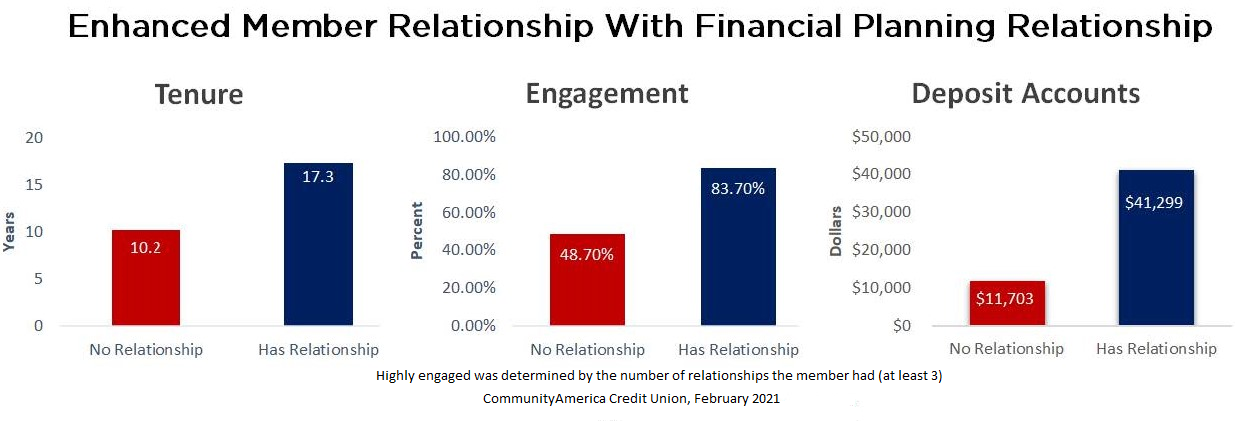

Research conducted by CommunityAmerica Financial Solutions, LLC (CAFS) supports these statements. They recently analyzed members’ relationships at CommunityAmerica Credit Union and CAFS found that members with a financial planning relationship with CAFS have increased tenure, engagement, and deposits with the credit union compared to members who do not have a financial planning relationship with CAFS.

CAFS has found that the average member tenure with a financial planning relationship is 17.3 years compared to 10.2 years on average for other members—an increase in tenure by 70%. And engagement statistics show the same path of increase. Members with a financial planning relationship are 83.7% highly engaged versus 48.7% engagement from those that do not have a financial planning relationship.

Deposit balances see an even more considerable increase. Members with a financial planning relationship have an average deposit balance nearly four times the deposits of those without a relationship. The average deposit balance for members with a financial planning relationship is $41,299 compared to the $11,703 average deposit balance for those without a financial planning relationship.

Even with these results, CAFS observes that 84% of members still do not have a documented financial plan, which means there is an opportunity for credit unions to provide financial planning as part of their members path to financial success.

So, this leads to the question of which members should have a plan? In the series of virtual dialogues we’ve moderated over the last several months, this question has come up frequently, and there are a wide range of responses.

Mike Haggerty, president of CAFS, believes, “There is no member relationship too big or too small not to have a financial plan.” However, many members do not choose to use a financial advisor because they feel they don’t have enough money to talk through planning and investments.

David Tuyo, President and CEO of University Credit Union (a CAFS partner), echoes Haggerty, “We serve students and those who are just graduating and acquiring various levels of debt, but then we also work with those who are further along in their careers with higher levels of income and who are planning for retirement. We want to make sure that we serve our members throughout their entire life and that we aren’t only serving them in their 20s or their 30s, but we’re serving them from start to finish. With this mindset, we have seen nice response rates from our membership around wealth management using us for the services.”

Tuyo goes on to say, “To make sure that members don’t go elsewhere for products and services that the Credit Union should be offering, start with education. We wanted our members to come to us for our expert advice; we believe that’s our core offering. It’s not checking accounts, car loans, mortgage loans, or wealth management; it is our expertise. That’s why they’re coming to us. Let’s face it, in today’s world, you can get any product or service needed online, and you can beat anybody’s rate just by going online. We want to be the professors for every member at every life stage.”

If you believe that every member should have a plan, it will take a while to get those created. The typical advisor in a credit union works with 2.1 members a month on a financial plan, including 1.2 new plans a month. That advisor has 538 member clients, so it would take almost 40 years to create a plan for all the advisor’s clients. This is why CAFS is partnering with credit unions to provide a fully digital and instant experience that is demanded by today’s members. By increasing efficiencies in setting up the basics, the advisor and member can have more meaningful interactions which includes having time to build financial plans that can help the member achieve their financial well-being.

But not every client needs a full plan. Some firms have introduced planning lite, which is coming to be called a “foundation” plan. For example, MoneyGuide has introduced Blocks, which enables an advisor to focus on a narrow member need, while assembling the framework to build a more comprehensive plan for the member, Block-by-Block.

While there are different answers to the question of who should have a plan, Kehrer Bielan’s Leigh Van Heule puts it in perspective— “You should do a plan with every client you want to keep.”

Join the conversation in our next virtual dialogues.

If you are a credit union and would like to learn more about how you can partner with CAFS, please contact the CAFS Chief Operating Officer, Justin Steitz, at jsteitz@CACU.com or (913) 905-8192.